Branches & agencies

Branches & agencies

News

Keep up to date with the latest from the Society – breaking news, helpful resources, updates to your products and services, supporting our wonderful community, and interesting blogs and stories.

-

The new face of H&R Online

Read more >: The new face of H&R Online -

Hinckley & Rugby appoints Chief Customer Officer

Read more >: Hinckley & Rugby appoints Chief Customer Officer -

Hospices receive another £21,000 thanks to Society savers

Read more >: Hospices receive another £21,000 thanks to Society savers -

Maximise your tax-free savings this ISA season!

Read more >: Maximise your tax-free savings this ISA season! -

The Society’s longstanding support for local theatre group continues with new production

Read more >: The Society’s longstanding support for local theatre group continues with new production -

Hinckley & Rugby goes nationwide with charity and business accounts

Read more >: Hinckley & Rugby goes nationwide with charity and business accounts -

It’s ISA season – make sure you don’t miss out!

Read more >: It’s ISA season – make sure you don’t miss out! -

Society appoints first female Chair of the Board

Read more >: Society appoints first female Chair of the Board -

Building Society Launches Competitive Savings Account for Existing Mortgage Customers

Read more >: Building Society Launches Competitive Savings Account for Existing Mortgage Customers -

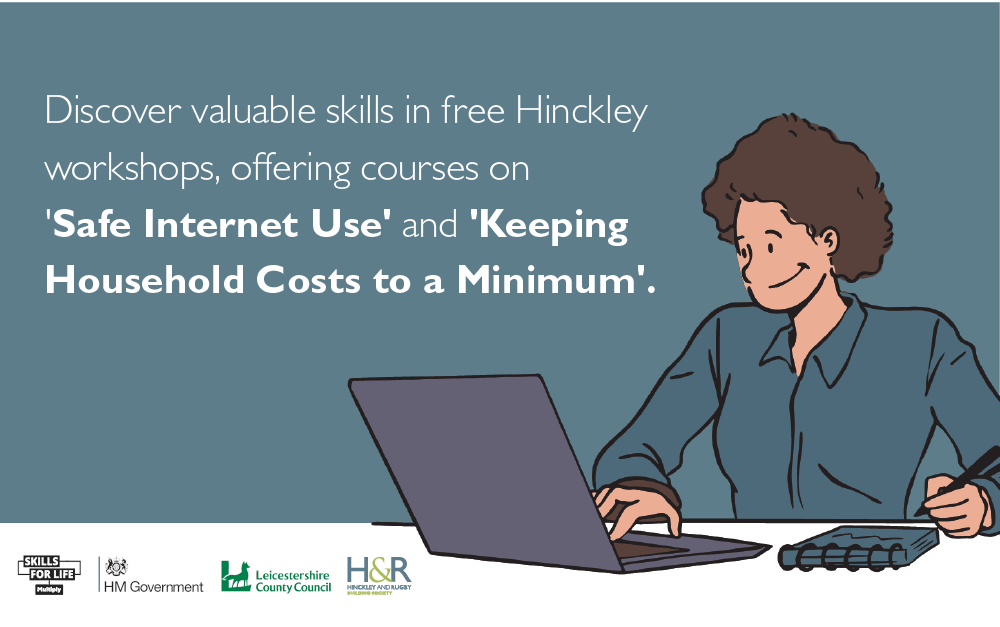

Numeracy programme to help adults build skills and gain confidence

Read more >: Numeracy programme to help adults build skills and gain confidence -

Savings made simple

Read more >: Savings made simple -

7 ways to improve your EPC rating

Read more >: 7 ways to improve your EPC rating

Not sure what you need?

Let us help

Explore our website to find what you need, or click below to get in touch with a member of our team.